Every trading day has a personality. The last one before the long Fourth of July weekend had two — and they barely spoke to each other. On one side, the Dow Jones printed yet another record close. On the other, semiconductors took their second beating in a row. In between, a soft jobs report poured fuel on the same fire that has driven markets for weeks: the great rotation of money out of tech and into the old-economy names.

The Day's Scoreboard

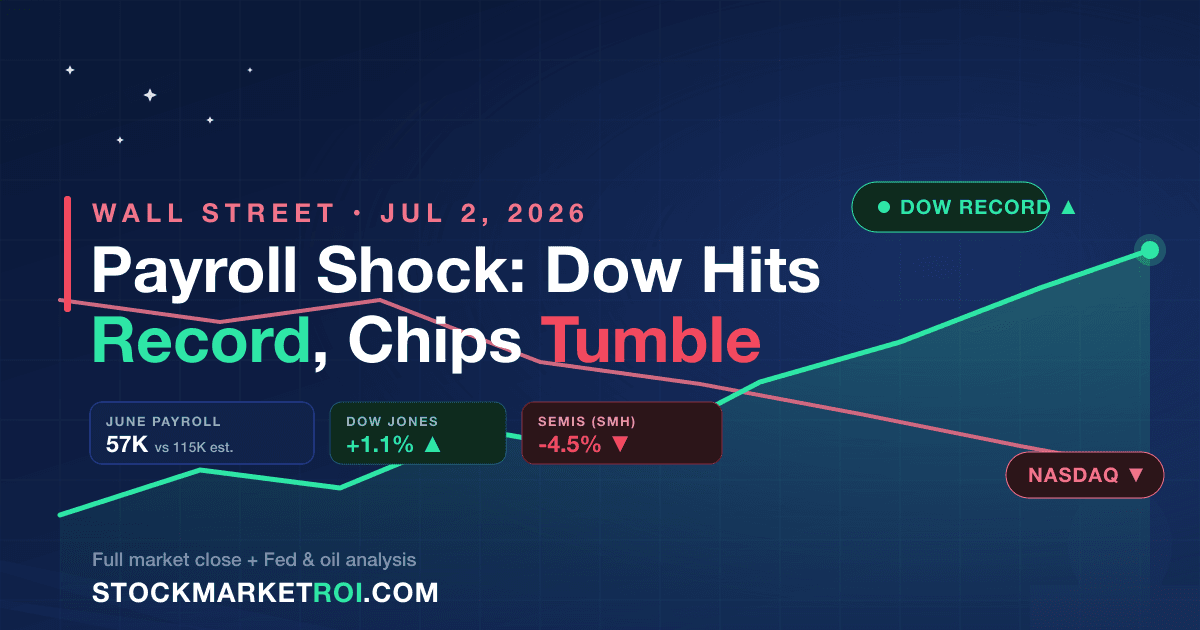

- Dow Jones: up about 1.1%, closing near 52,900 — a fresh record close. The only major index to rally with conviction.

- S&P 500: essentially flat, around 7,483, caught between strength in defensives and weakness in tech.

- Nasdaq Composite: down roughly 0.8%, near 25,830, hammered by another day of chip selling.

- Russell 2000: off about 0.5% (2,996). The VIX fear gauge slipped to about 16 — no panic here.

The split has a name: while Apple surged +4.8% and carried the Dow almost single-handedly, Tesla cratered and the chip complex melted. Two markets, one day.

Anatomy of the June Jobs Report

The Bureau of Labor Statistics reported just 57,000 nonfarm payrolls in June — well below the 115,000 consensus and a sharp slowdown from May's downwardly-revised 129,000. The hole came from leisure and hospitality, which shed 61,000 jobs; on the plus side, professional and business services (+36,000), social assistance (+25,000) and healthcare (+22,000) carried the load. Average hourly earnings rose 0.3% to $37.64.

The unemployment rate, paradoxically, fell to 4.2% from 4.3%. The trick sits in the labor-force participation rate, which dropped 0.3 point to 61.5% — the lowest since March 2021. Translation: people stopped looking for work and fell out of the count. A labor market cooling from underneath, not heating up.

What It Means for Kevin Warsh's Fed

Here is the day's most important read — and it is different from the 2024/2025 cycle. The Fed, now chaired by Kevin Warsh, had been hawkish: with rates near 3.6%, markets had actually priced a possible hike (not a cut) as soon as September. Speaking in Sintra on July 1, Warsh acknowledged inflation is still too high but conceded the risks had eased over recent weeks.

The weak payroll nudges that board: a cooling labor market reduces the urgency to tighten further. Add oil back at pre-conflict levels, and the base case shifts from "hike in September" to "rates on hold." And for stocks, swapping "rates rising" for "rates steady" is fuel — exactly what rate-sensitive sectors celebrated.

The Great Rotation: Why the Dow Rises as the Nasdaq Falls

It is the move strategists have been calling the Great Rotation: money leaving fast-growth stories — tech and AI, which soared in the first half — and rotating into value and dividends, the meat-and-potatoes that dominate the Dow.

The chip selloff was the epicenter. The VanEck Semiconductor ETF (SMH) fell about 4.5%, its second straight day of heavy profit-taking. The day's laggards, at the close:

| Company | Ticker | On the Day | Context |

|---|---|---|---|

| Teradyne | TER | -13.6% | Selloff in chip-test equipment |

| KLA Corp. | KLAC | -11.5% | Profit-taking after a historic run |

| Intel | INTC | -5.3% | Dragged down with the group |

| Micron | MU | -5.5% | Sharp pullback, still a top gainer this year |

| AMD | AMD | -4.3% | Profit-taking |

| Broadcom | AVGO | -2.4% | Heavyweight under pressure |

| NVIDIA | NVDA | -1.4% | Held up better than peers |

The drivers: stretched valuations after a historic half, doubts about the sustainability of AI capex, and the classic profit-taking ahead of a three-day weekend. Want to slice it sector by sector? Run a quick filter on our stock screener.

Tesla: Record Deliveries, Stock in the Mud

Tesla delivered 480,126 vehicles in the second quarter — a record for any Q2, up 25% from about 384,000 a year ago and well above the roughly 406,600 consensus. Model 3 and Model Y accounted for 467,762 units, on production of 451,758.And yet the stock fell about 7.5%. Why? The market has already looked past deliveries: the question now is margins, and that answer only comes with the July 22 earnings report. It is the perfect snapshot of a session where good tech news was not enough — it got sold anyway.

Oil Back to Pre-Conflict Levels

The other big macro story came from crude. WTI slid to about $68.5 a barrel, its lowest since late February; Brent hovered near $70–71. In other words, the risk premium from US/Israel–Iran tensions has been almost entirely unwound.

The reasons: indirect U.S.–Iran talks in Qatar, with President Donald Trump praising the progress; and a normalizing Strait of Hormuz, where flows now top 10 million barrels a day — with the UAE restoring exports above 3.9 million barrels daily into an oversupplied market. The sticking point that still blocks a final deal: Tehran continues to demand maritime control of the strait. Per reports, the next round of talks was delayed by the funeral of former Supreme Leader Ali Khamenei, beginning July 4. For U.S. inflation — and the Fed — oil at $68 instead of $100+ is the best disinflationary gift there is.

The Backdrop: The Best First Half in Years

Remember where the market is coming from. In the first half of 2026:

- Dow: +8.85% — best first half since 2021

- S&P 500: +9.55%

- Nasdaq: +12.79%

- Russell 2000: +21.86% — its strongest first half since 1991

Against that backdrop, the chip correction reads far more like healthy profit-taking inside a bull market entering its fourth year than a trend reversal.

The Calendar: Holiday and What to Watch

- Friday, July 3: the NYSE and NASDAQ are closed for the observed Independence Day holiday, since July 4 falls on a Saturday. Bonds had an early close Thursday and are shut Friday. Full reopen is Monday, July 6. See our full market calendar.

- SpaceX into the Nasdaq-100: it joins before the July 7 open, with index funds buying after the July 6 close. It is the fastest inclusion in the benchmark's history — 15 trading days after its IPO — with JPMorgan estimating about $4.3 billion in forced buying.

- Chips and the Fed: whether the semiconductor selloff continues after the break, and how the rates market re-prices the weak payroll.

Frequently Asked Questions

How many jobs did the U.S. add in June 2026?

The U.S. added 57,000 nonfarm payrolls in June 2026, well below the 115,000 consensus. May was revised down to 129,000.

Why did unemployment fall if hiring was weak?

Because the labor-force participation rate dropped 0.3 point to 61.5%, the lowest since March 2021. People who stop looking for work leave the official unemployment count, which can pull the rate down even when hiring is soft.

Is the U.S. stock market open on Friday, July 3, 2026?

No. The NYSE and NASDAQ are closed for the Independence Day holiday, since July 4 falls on a Saturday.

Did Tesla rise on its record deliveries?

No. Despite a record 480,126 deliveries, up 25%, Tesla stock fell about 7.5%, with investors focused on margin uncertainty ahead of the July 22 earnings report.

Why did the Dow rise while the Nasdaq fell on the same day?

Capital rotation: investors took profits in technology, especially semiconductors, and moved into value and dividend names that dominate the Dow, with Apple up 4.8% leading the index higher.

Disclaimer: This content is for informational and educational purposes only and is not investment advice. Figures refer to the July 2, 2026 session and may be subject to official revisions. Past performance does not guarantee future results. Consult a certified professional before making financial decisions.